Industry research

Pediatric care services

Scope

US

Companies

71

Key takeaways

What is the scope of this industry report?

The US pediatric care services industry comprises clinics, hospitals, therapy centers and home-based care providers that provide comprehensive medical, preventive and developmental care for infants, children and adolescents. These services include general pediatric care, which focuses on routine health monitoring, preventive services and treatment of common childhood illnesses. Whereas, specialized care service providers focus on specific pediatric subspecialties that address complex conditions or targeted therapeutic needs,

What does the Pediatric care services landscape look like in US?

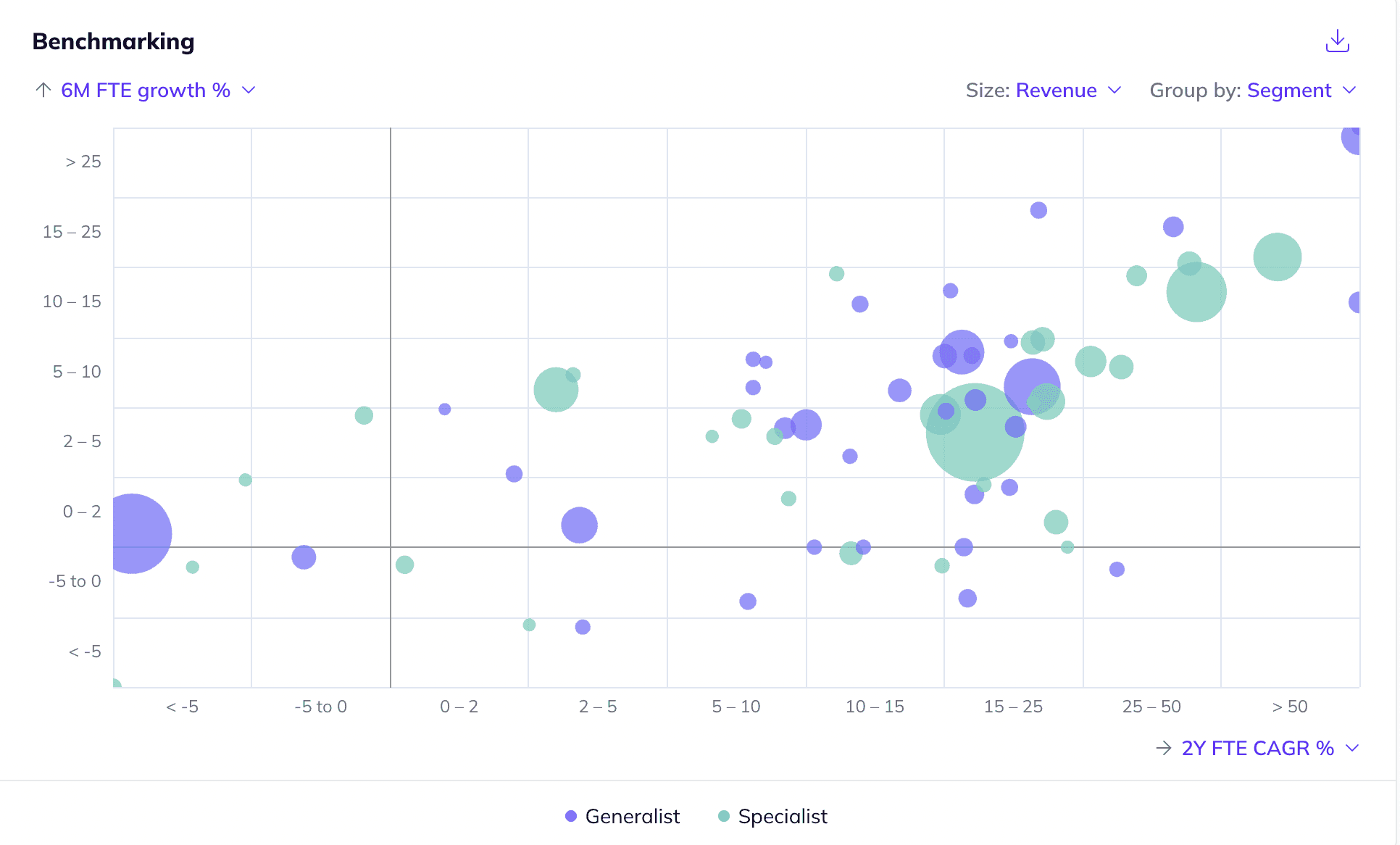

The competitive landscape in the US pediatric care services industry remains highly fragmented across both generalist and specialist segments. Herein, pure-play pediatric practices face competition from large multispecialty healthcare organizations that maintain dedicated pediatric service lines, such as Mayo Clinic (US) and Envision Physician Services (US). Additionally, incumbents compete with large nonprofit pediatric hospital systems, including Children's Hospital of Philadelphia (US), Texas Children's Hospital (US), Cincinnati Children's Hospital Medical Center (US) and Boston Children's Hospital (US). Large pure-play pediatric care providers compete through scale advantages, which support centralized administrative functions, stronger payer contracting leverage and broader geographic coverage. To compete, the long tail differentiates itself through a focus on a particular geography to build strong patient relationships and improve retention. At the same time, consolidation continues across the industry as providers look to achieve scale amid lagging reimbursement and rising operating costs, with PE firms forming platform companies that support practice roll-ups.

What does the Pediatric care services market landscape look like in US?

Investor-led interest has been moderate, with ~33% of identified assets being backed by financial sponsors (as of March 2026). Investors are primarily attracted by the market's favorable long-term outlook on the back of (i) the rising prevalence of pediatric chronic and developmental conditions, (ii) simplification of insurance administration and Medicaid processes, which improves operational efficiency and (iii) the emergence of digital health technologies that improve diagnosis, care coordination and treatment outcomes. On the other hand, deterring factors include (i) declining US birth rates that reduce the size of the pediatric patient population and potential demand for care services, (ii) adverse reimbursement shifts, federal research funding uncertainty and an increase in operating costs and (iii) workforce shortages in pediatric medicine that increase staffing costs and constrain service capacity.

What are the key ESG considerations in US's Pediatric care services industry?

ESG topics in the US pediatric care services industry primarily relate to environmental and social challenges. Herein, environmental concerns stem mainly from high energy and water use across outpatient clinics and therapy centers, as well as from the use of single-use plastics and disposable medical supplies that generate clinical waste. To mitigate these impacts, incumbents implement energy-efficiency programs, water conservation initiatives and waste segregation and recycling measures to improve resource efficiency across clinical operations. From a social perspective, disparities in access to pediatric care, patient safeguarding and clinician burnout remain key concerns. To address these issues, incumbents expand telehealth and in-home care models to improve accessibility, introduce clinician training and workforce support programs to strengthen staff retention and capacity and enforce strict child-protection protocols, including staff background checks, abuse-reporting procedures and clinical supervision, to ensure safe care delivery for minors.

Company benchmarking

Market growth

Technavio (November 2024) estimates that the global autism spectrum disorder market generated ~$7.8bn in revenue in 2024 and expects it to reach ~$11.2bn by 2029 (+7.6% CAGR 2024-2029)

The US autism treatment market is projected to grow from ~$4.7bn in size in 2023 to ~$6.5bn by 2028 (+6.7% CAGR 2023-2028; Hyde Park Capital, March 2024)

Positive drivers

Rising prevalence of pediatric chronic and developmental conditions such as asthma, diabetes, cancer and neurodevelopmental disorders (e.g. autism, ADHD) are expected to drive sustained growth. To illustrate, one-third of the US youth population lives with a chronic health condition, while the number of young people (i.e. under 20) with type 1 or type 2 diabetes expected to double by 2060 (vs. 2024; UCLA Health, March 2025; CDC, May 2024)

Regulatory initiatives that simplify insurance administration and cross-state Medicaid processes may support improved operational efficiency across the pediatric care services industry. For instance, the Accelerating Kids’ Access to Care Act aims to streamline Medicaid enrollment and authorization procedures across states, which may reduce administrative complexity and enable faster access to specialized pediatric care for children with complex medical needs who require treatment from out-of-state providers (AAP News, March 2026; Financial Times, April 2025)

The emergence and advancement of digital health technologies such as AI, telemedicine and remote monitoring improve diagnostic accuracy, care coordination and treatment outcomes in pediatric healthcare settings. To illustrate, AI-based imaging tools in pediatric radiology achieve diagnostic accuracy of ~87% and sensitivity of ~84% across multiple imaging applications (Journal of Neonatal Surgery, February 2025; MDPI, March 2023)

Negative drivers

Declining birth rates in the US reduce the size of the pediatric patient population, which may lead to lower demand for care services and constrain long-term growth for pediatric care providers. To illustrate, the US Census Bureau projects that the total US pediatric population and patient base will decrease by ~5% between 2025-2040 (AAMC, February 2026; JHU, January 2026; EY, September 2025)

Adverse shifts in reimbursement models, uncertainty around federal research funding and an increase in operating costs place significant financial pressure on the US pediatric care services industry. These risks are particularly acute due to the sector’s high reliance on public payers, as Medicaid covers roughly half of all patients treated at children’s hospitals, while potential reductions of ~$1tn in Medicaid funding over the next decade may further constrain revenue growth and margins (Pathstone Partners, February 2026; EY, September 2025; Chartis, September 2025)

Workforce shortages in pediatric medicine increase staffing costs and operational strain for care providers, which limits service capacity and constrains their ability to meet patient demand. To illustrate, the US healthcare industry is estimated to face a ~14% reduction in pediatric primary-care physicians by 2037 (i.e. vs 2023; NASHP, January 2026; HRSA, December 2025; AAMC, September 2024)

Fill out the form to request your copy of the Pediatric care services industry report

With the full report, you’ll gain access to:

Detailed assessments of the market outlook

Insights from c-suite industry executives

A clear overview of all active investors in the industry

An in-depth look into 71 private companies, incl. financials, ownership details and more.

A view on all 130 deals in the industry

ESG assessments with highlighted ESG outperformers

Discover hundreds of niche industry reports on Gain

Deep dive into additional industries to understand their market outlook, positive and negative drivers, and more!