Industry research

InsurTech

Scope

US

Companies

48

Key takeaways

What is the scope of this industry report?

The US InsurTech industry comprises businesses that develop and deploy technology to modernize and digitize the insurance value chain, spanning from risk assessment and underwriting to policy administration, distribution and claims handling. Within this landscape, a subset of players (e.g. Guidewire Software, Duck Creek Technologies) operate as technology vendors, providing SaaS platforms with AI-driven analytics and workflow automation tools to insurance carriers, thereby managing general agents (MGAs) and brokers without taking on underwriting risk or participating in distribution. By contrast, another cohort (e.g. Cover Genius, Sure) combines proprietary software platforms with active participation in insurance distribution, facilitating policy issuance through carrier licenses, MGA structures or embedded partnerships. As such, we have segmented the US InsurTech market by value chain participation into: (i) B2B SaaS and (ii) insurance distribution platforms.

What does the InsurTech landscape look like in US?

Revenue generation across the US InsurTech market varies materially by business model, with monetization structures ranging from recurring software subscriptions to usage-based fees and distribution-linked income. Within the B2B SaaS segment, the industry standard remains rooted in SaaS subscriptions or term licensing, whereby vendors (e.g. Guidewire Software) charge carriers, MGAs and brokers recurring annual fees for platform access (Guidewire Software, September 2024). Additionally, some software players supplement or replace subscription fees with per-unit pricing tied directly to platform usage. For example, AgentSync charges insurance carriers and agencies a fee for each licensed agent actively managed on its compliance platform, with average annual contract values of ~$100k (Vendr, April 2025; StartupTalky, March 2023). In the software and distribution segment, revenue extends beyond software fees to include distribution-linked income tied to policy issuance, such as earned premiums, commissions and revenue shares with carrier and merchant partners. To illustrate, Cover Genius embeds insurance products directly into the checkout flows of digital platforms such as eBay (US) and Booking Holdings (US), earning a revenue share on every policy sold through those partners' platforms (AlleyWatch, May 2024).

What does the InsurTech market landscape look like in US?

The US InsurTech market remains fragmented, as players tend to specialize across distinct segments of the insurance value chain, whether by workflow function (e.g. underwriting automation, claims management, fraud detection), line of business or end-market vertical. Within the P&C sector, the largest contributor to industry net premiums written, the leading players include Guidewire Software, Duck Creek Technologies and Insurity (Practo Insura, September 2025; Businesswire, April 2023). These players capture market share by building broad, integrated platforms that serve as a system of record across the insurance value chain, creating high switching costs for carrier clients. To illustrate, Guidewire Software serves >570 P&C insurers across ~43 countries through an integrated cloud platform spanning core systems, data analytics, digital tools and AI. The scale of its operations, backed by >1.7k successful implementations, makes displacement highly complex (Guidewire Software, September 2025). Despite this structural entrenchment, players in this industry face competition from enterprise software incumbents such as Salesforce (US), Microsoft (US), SAP (GE), Oracle (US) and IBM (US), which deploy insurance-specific modules atop horizontal platforms to compete directly with specialist InsurTech vendors (Microsoft, April 2026; SAP, April 2026; Salesforce, October 2024). At the same time, InsurTech players increasingly face disintermediation risk from incumbent insurance carriers that acquire proprietary technology platforms to reduce reliance on third-party vendors. To illustrate, The Travelers Companies acquired Trōv’s on-demand, API-based embedded insurance platform and completed a ~$435m acquisition of Corvus Insurance Holdings, bringing in-house AI-driven cyber underwriting, risk scoring and vulnerability scanning capabilities (Insurance Journal, January 2024; Travelers, November 2023; Insurance Journal, February 2022). As a result, some players pursue strategic acquisitions to broaden their platform capabilities and pre-empt competitive displacement. For example, Applied Systems completed 3 acquisitions between 2022 and 2025, acquiring Tarmika (commercial lines rating platform), Planck (AI underwriting platform) and Cytora (risk digitization platform), progressively extending its coverage of the end-to-end insurance distribution workflow (Coverager, September 2025; Applied Systems, August 2022).

What are the key ESG considerations in US's InsurTech industry?

Sponsor-led interest has been high, with ~86% of identified assets being sponsor-backed (as of April 2026). Factors that attract investors include (i) integration of machine learning that improves underwriting precision and operational productivity, (ii) convergence of embedded insurance and digital-first distribution that expands the addressable market, as well as (iii) rising complexity of risk which increases demand for advanced analytics and real-time data capabilities. Deterring factors for investment primarily relate to (i) fragmented state-level regulations impeding national scale opportunities, (ii) a structural deficit in labor slowing down adoption and implementation, as well as (iii) interoperability challenges across siloed legacy architectures extending deployment timelines.

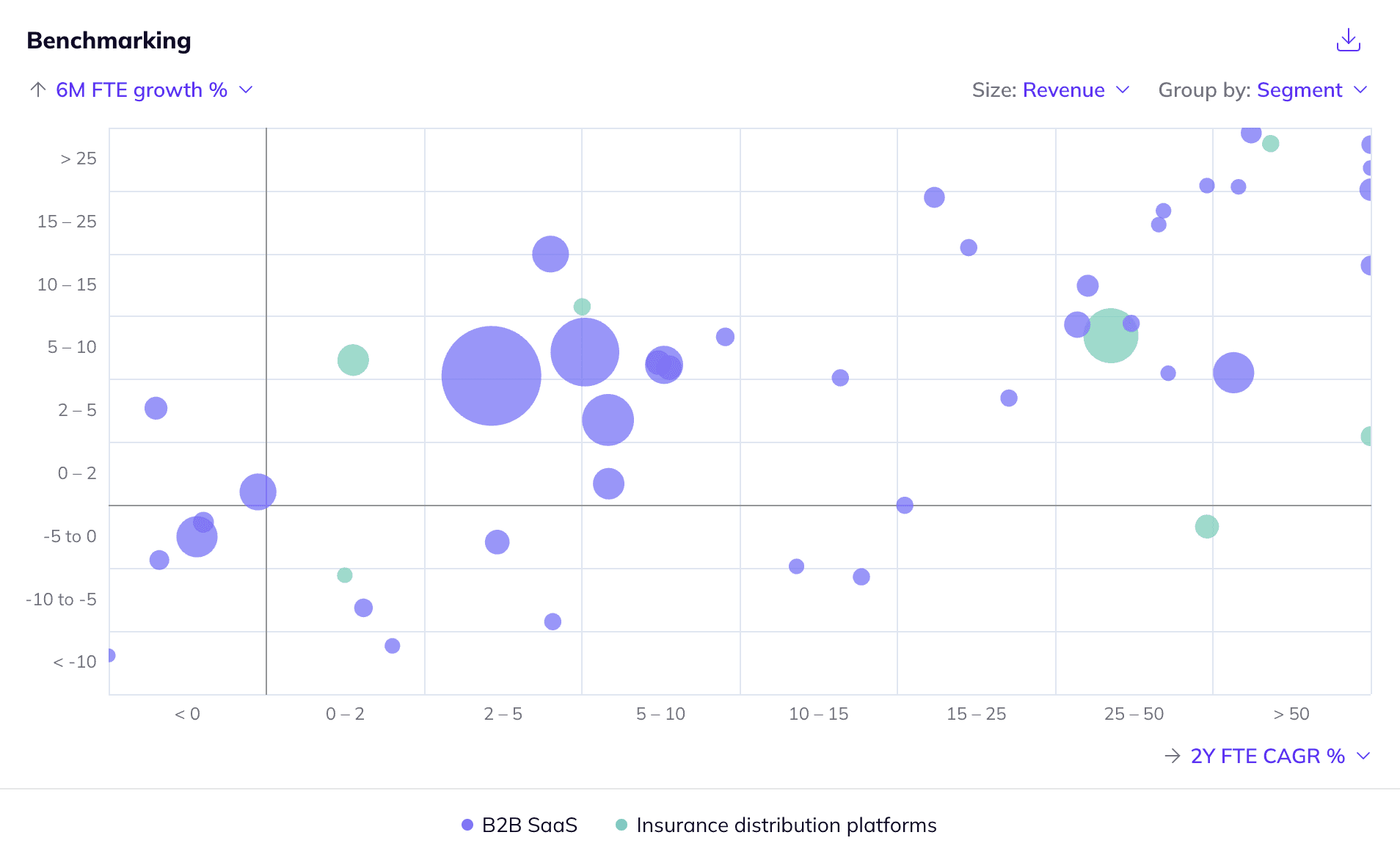

Company benchmarking

Market growth

The fee-based revenue for US P&C insurers will grow from ~$21.6bn in 2023 to ~$49.5bn by 2030 (+12.55% 2023-2030 CAGR; Deloitte, April 2025)

According to Houlihan Lokey (March 2026), InsurTech software spending across North America is projected to rise from ~$38.4bn in 2024 to ~$74.0bn by 2029 (+14.0% CAGR 2024-2029)

Positive drivers

The integration of machine learning-based policy decisioning and claims automation into core insurance processes will significantly improve underwriting precision and operational productivity. McKinsey & Company (July 2025) estimates that GenAI could generate between ~$50-70bn in additional insurance industry revenue by automating complex document analysis and hyper-personalizing customer interactions (Reinsurance News, February 2026)

The convergence of embedded insurance and digital-first distribution structurally expands the addressable market by capturing demand at the point of sale through enhanced convenience and price transparency. Embedded insurance is expected to account for ~25% of the total global P&C insurance market by 2030, while digital auto insurance purchases have reached ~47%, officially surpassing agent-led transactions (J.D Power, May 2025; Carrier Management, May 2025; KPMG, April 2024)

Rising complexity of risk, particularly from climate catastrophes and cyber exposures, increases demand for advanced analytics and real-time data capabilities. The growing frequency and severity of these risks push insurers to adopt more sophisticated data-driven approaches to pricing and risk management (Ambee, February 2026; AON, October 2025; McKinsey & Company, July 2024; CapitalMonitor, December 2022)

Negative drivers

Fragmented state-level regulations in the US continue to impede the rapid scaling of standardized digital insurance products. Each state maintains its own licensing requirements and rate-filing rules, forcing InsurTechs to navigate 50 distinct regulatory frameworks to achieve national coverage. These administrative complexities often delay product launches by ~12-18 months, draining the capital of players in the industry (Insurance Edge, February 2026; Guidewire, December 2025; Genasys, August 2025)

A structural deficit in digital, data science and AI-skilled labor strains the pace at which carrier clients can integrate and operationalize InsurTech offerings. Carriers face intensifying competition for data science and actuarial talent from technology companies, eroding the human capital needed to deploy and sustain modern InsurTech platforms at scale (DataBricks, November 2025; Insurance Journal, March 2025; Deloitte, September 2023)

Interoperability challenges across siloed legacy architectures materially extend InsurTech deployment timelines. BCG's analysis found that ~35% of all insurance applications still run on legacy technology stacks that are not cloud-ready, while McKinsey & Company notes that even commercial off-the-shelf platform implementations frequently require extended integration timelines due to product complexity and bespoke process customization (Genasys, February 2026; McKinsey & Company, May 2025; BCG, May 2024)

Fill out the form to request your copy of the InsurTech industry report

With the full report, you’ll gain access to:

Detailed assessments of the market outlook

Insights from c-suite industry executives

A clear overview of all active investors in the industry

An in-depth look into 48 private companies, incl. financials, ownership details and more.

A view on all 264 deals in the industry

ESG assessments with highlighted ESG outperformers

Discover hundreds of niche industry reports on Gain

Deep dive into additional industries to understand their market outlook, positive and negative drivers, and more!