Industry research

Low-code and no-code platforms

Scope

US

Companies

197

Key takeaways

What is the scope of this industry report?

The US low-code and no-code platforms market comprises players that enable application development and workflow automation through drag-and-drop interfaces, pre-built component libraries and reusable logic. Unlike traditional software development, which requires extensive manual coding, multi-month delivery cycles and dedicated engineering resources, LCNC platforms allow both technical and non-technical users to build and deploy functional software in a fraction of the time and cost. Herein, some players specialize in the design, configuration and deployment of standalone applications using visual development environments. While others help organizations connect software systems, automate workflows and manage data movement across existing technology environments, rather than building new user-facing applications.

As such, we segmented the US low-code and no-code (“LCNC”) platforms market into:

Application development platforms,

Automation, integration and analytics platforms.

What does the low-code and no-code landscape look like in the US?

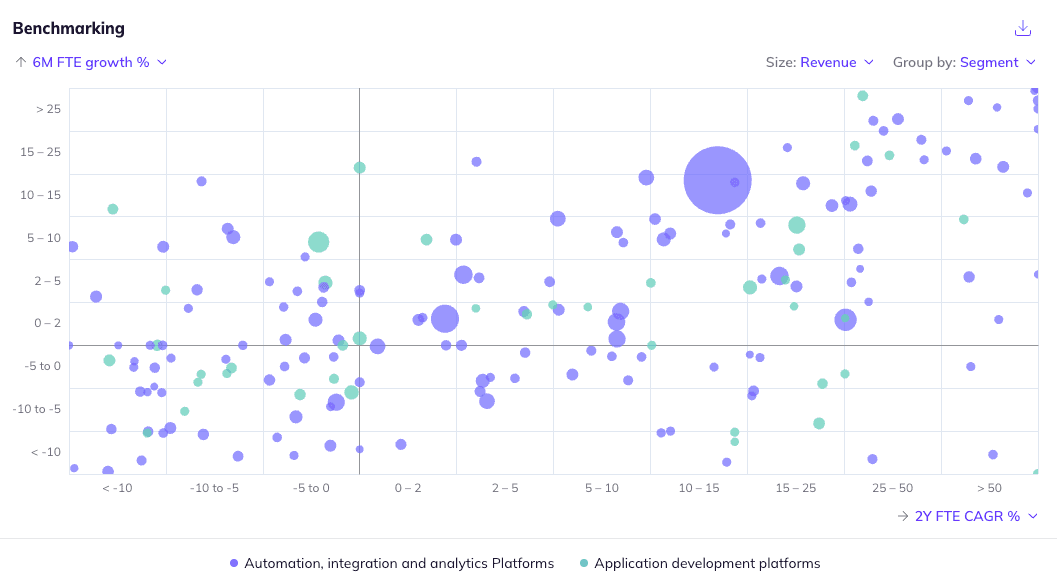

The competition in the overall US low-code and no-code platforms market varies across the two segments. The application development market reflects a bifurcated structure, with a small cluster of scaled enterprise and mid-market platforms such as Appian, Airtable and Webflow alongside a highly fragmented long tail of players targeting SMBs and citizen developers. Larger players capture market share by investing in regulatory accreditations and security certifications that smaller no-code rivals cannot replicate, qualifying the larger players to handle high-compliance workloads in regulated industries and the federal government. However, players in this segment face growing pressure from generative AI coding tools such as GitHub Copilot (Microsoft, US), Cursor (Anysphere, US) and Claude Code (Anthropic, US), which enable technically proficient users to build applications directly from natural language prompts. Competitive pressure is therefore shifting from basic ease of use toward platform differentiation, as the convergence of AI-generated code and visual development pushes LCNC platforms to embed native AI capabilities across design, build, testing and optimization workflows. On the other hand, the automation, integration and analytics segment remains structurally fragmented, with scale leaders emerging within distinct sub-verticals such as system integration (e.g. Boomi), workflow and business process automation (e.g. ServiceNow), test automation (e.g. Tricentis) and embedded analytics (e.g. ThoughtSpot). The segment faces structural competition from large technology incumbents such as Microsoft (Power Platform, US) and Oracle (Oracle Integration Cloud, US), which bundle automation and integration capabilities within broader enterprise contracts. Indirect competitive pressure also comes from managed service providers (MSPs) such as Accenture (IE), Cognizant (US) and IBM (US), which manage software workflows and system connectivity for customers, particularly mid-market organizations with limited technical resources.

What does the low-code and no-code market landscape look like in the US?

Sponsor-led interest has been high, with ~78% of identified assets being sponsor-backed (as of May 2026).

Factors that attract investors include:

Convergence of Gen AI with LCNC platforms, which significantly accelerates development cycles while broadening platform capabilities,

Adoption for enterprise modernization and mission-critical workflows expected to support long-term market growth,

Structural shortage of software engineering talent in the US supporting long-term demand.

On the other hand, deterring factors include:

Escalating competition for discretionary IT budgets expected to constrain enterprise spending,

Scalability limitations in complex, performance-intensive workloads may restrict LCNC adoption across certain enterprise applications,

Commoditization of basic automation and application-building features within broader enterprise software suites may reduce pricing power and differentiation.

What are the key ESG considerations in the low-code and no-code industry?

ESG topics in the US low-code and no-code platforms market primarily span environmental and governance factors. From an environmental perspective, cloud-hosted LCNC platforms rely entirely on data center infrastructure, which carries a meaningful and growing carbon footprint. To mitigate this risk, players rely on lower-carbon cloud infrastructure and renewable energy sourcing to reduce data center-related emissions. Additionally, the rapid embedding of generative AI capabilities into LCNC platforms compounds this challenge by materially escalating per-task compute intensity. To limit redundant compute overhead, some platforms embed structured AI governance frameworks that include model retirement protocols and auditable deployment practices. From a governance perspective, LCNC platforms can support more effective ESG reporting by simplifying the integration and management of complex and multi-source data. This enables stronger governance outcomes without diverting scarce skilled developers from core and high-value initiatives. At the same time, applications built by citizen developers are frequently created without robust IT governance, increasing the likelihood of security vulnerabilities and exposing organizations to potentially substantial financial losses. In response, platforms invest in enterprise-grade security certifications and embedded governance controls to provide audit trail visibility and access management.

Company benchmarking

Market growth

The global low-code development platform market was valued at ~$19.4bn in 2024 and is expected to reach ~$109.1bn by 2029 (+41.3% CAGR 2024-2029; Technavio, May 2025)

Gartner estimates new enterprise applications that will be developed with low-code technologies to increase from ~25% in 2020 to ~75% by 2026 (Kissflow, May 2026)

Positive drivers

The convergence of generative AI with LCNC platforms significantly accelerates development cycles while broadening platform capabilities, reinforcing long-term platform relevance over standalone AI coding tools. To illustrate, AI copilots reduce LCNC development time by up to 40% (Phoenix DX, November 2024)

Enterprise workflow modernization and legacy system replacement are expected to support long-term LCNC adoption, as organizations increasingly seek faster and more cost-efficient ways to digitize processes and connect fragmented software environments. This supports demand for platforms that reduce reliance on time-intensive custom development while improving operational flexibility (TechTarget, March 2024)

The structural shortage of software engineering talent in the US supports long-term demand for LCNC platforms, as enterprise software needs outpace workforce expansion. This supply-demand gap strengthens the case for LCNC platforms, enabling non-technical users to build and automate applications while reducing reliance on scarce engineering resources, lowering development costs and shortening delivery timelines (CompTIA, March 2024; The Economic Times, March 2026)

Negative drivers

Escalating competition for discretionary IT budgets is expected to constrain enterprise LCNC spending, as software cost inflation and higher AI expenditures reduce funding available for new platform purchases. For instance, Gartner reports CIOs anticipate ~8.9% cost inflation for existing IT products and services in 2025, increasing pressure on LCNC vendors to demonstrate near-term ROI and justify procurement within tighter budget cycles (Gartner, October 2024)

Scalability limitations in complex, performance-intensive workloads may restrict LCNC adoption across certain enterprise applications. Herein, constraints around real-time processing, concurrency and deployment flexibility may limit LCNC adoption in latency-sensitive sectors such as manufacturing, aerospace and financial services (Forbes, March 2026)

Growing commoditization of basic automation and application-building features may pressure standalone LCNC platforms, as capabilities such as drag-and-drop workflow creation and AI-assisted development become increasingly embedded within broader enterprise software suites. This may weaken differentiation for standalone platforms and create pressure on pricing power (DEVOPSdigest, January 2024)

Fill out the form to request your copy of the Low-code and no-code platforms industry report

With the full report, you’ll gain access to:

Detailed assessments of the market outlook

Insights from c-suite industry executives

A clear overview of all active investors in the industry

An in-depth look into 197 private companies, incl. financials, ownership details and more.

A view on all 899 deals in the industry

ESG assessments with highlighted ESG outperformers

Discover hundreds of niche industry reports on Gain

Deep dive into additional industries to understand their market outlook, positive and negative drivers, and more!