Executive Summary

Welcome to the first edition of the M&A 50 report. In this report, we rank and analyze the largest and most active M&A advisors to private equity sponsors across the transatlantic markets.

Our ranking is based on total deal value advised to PE sponsors in 2025, covering entries, exits, and add-ons. We exclude IPOs and ECM activity.

Key takeaways from our analysis:

J.P. Morgan has emerged as the largest M&A advisor to PE sponsors, advising on $364.3bn across 95 transactions in 2025, followed by Goldman Sachs ($347.1bn, 103 deals) and Morgan Stanley ($264.1bn, 67 deals). Other advisors in the top 10 include Evercore ($181.6bn), Bank of America ($149.7bn), Jefferies ($139.2bn), UBS ($132.1bn), Deutsche Bank ($123.5bn), Citi ($120.0bn), and RBC Capital Markets ($115.3bn).

US HQ'd advisors dominate the M&A 50 ranking, capturing 26 of the top 50 spots. Europe has 18 advisors in the ranking, with representation coming mainly from the UK (7 advisors) and France (6).

TMT is the largest sector of advisory by the M&A 50, accounting for 27% of deal value, followed by Services (13%), Energy & Materials (12%) and Science & Health (12%). By region, the US dominates, accounting for 64% of total advised deal value.

US advisory activity is dominated by US-headquartered advisors, holding a steady ~85% share across all deal sizes, with limited presence from international advisors. In Europe, the market is more fragmented between local and US advisors, with US firms commanding a rising share as deal size grows, reaching 54% for large-cap deals.

By deal count, Houlihan Lokey (187), Lincoln International (133), and Jefferies (126) rank as the most active advisors. Rothschild & Co (115) is the most active non-US advisor. On average, a top 50 advisor closed 45 deals at an average deal value of $1.6bn.

Chapter 01: The M&A 50

J.P. Morgan has emerged as the largest M&A advisor to PE sponsors. It advised on 95 transactions (including entries, exits, and add-ons) for a total deal value of $364.3bn in 2025.

Closely following J.P. Morgan are Goldman Sachs ($347.1bn, 103 deals) and Morgan Stanley ($264.1bn, 67 deals). Other M&A advisors in the top 10 include Evercore ($181.6bn), Bank of America ($149.7bn), Jefferies ($139.2bn), UBS ($132.1bn), Deutsche Bank ($123.5bn), Citi ($120.0bn), and RBC Capital Markets ($115.3bn).

On average, the top 50 M&A advisors advised on 45 deals each, with an average deal value of $1.6bn.

By deal count, Houlihan Lokey (187), Lincoln International (133), and Jefferies (126) ranked as the most active investors.

The table below lists all the top 50 M&A advisors to PE. Use the search bar or the arrows at the top to navigate through the ranking.

Insights

US HQ'd advisors dominate the M&A 50 ranking, capturing 26 of the top 50 spots. Europe has 18 advisors in the ranking, with representation coming mainly from the UK (7 advisors) and France (6). Beyond this, presence is thin: Italy has 2 (Mediobanca and Intesa Sanpaolo), Germany, Switzerland, and Spain have 1 each in Deutsche Bank, UBS, and Santander respectively, and no Benelux HQ'd advisor features in our top 50 ranking. The remaining spots are split between Canadian advisors (RBC, TD Securities, and BMO) and APAC HQ'd firms including Mizuho, Macquarie, and Nomura.

TMT is the largest sector of advisory by the M&A 50, accounting for 27% of deal value, followed by Services (13%), Energy & Materials (12%) and Science & Health (12%). By region, the US dominates, accounting for 64% of total deal value, reflecting the bigger fee pool and larger transaction sizes compared to Europe.

The top 10 advisors are more US-heavy (58% for top 10 vs. 48% overall), while advisors ranked 31-50 show greater UK&I (19%) and France (12%) exposure. By sector, the top 10 advisors lean more toward Financial Services (14% vs. 8% overall). Services exposure, in contrast, increases lower down the ranking, rising from 19% for the top 10 to 32% for advisors ranked 31-50.

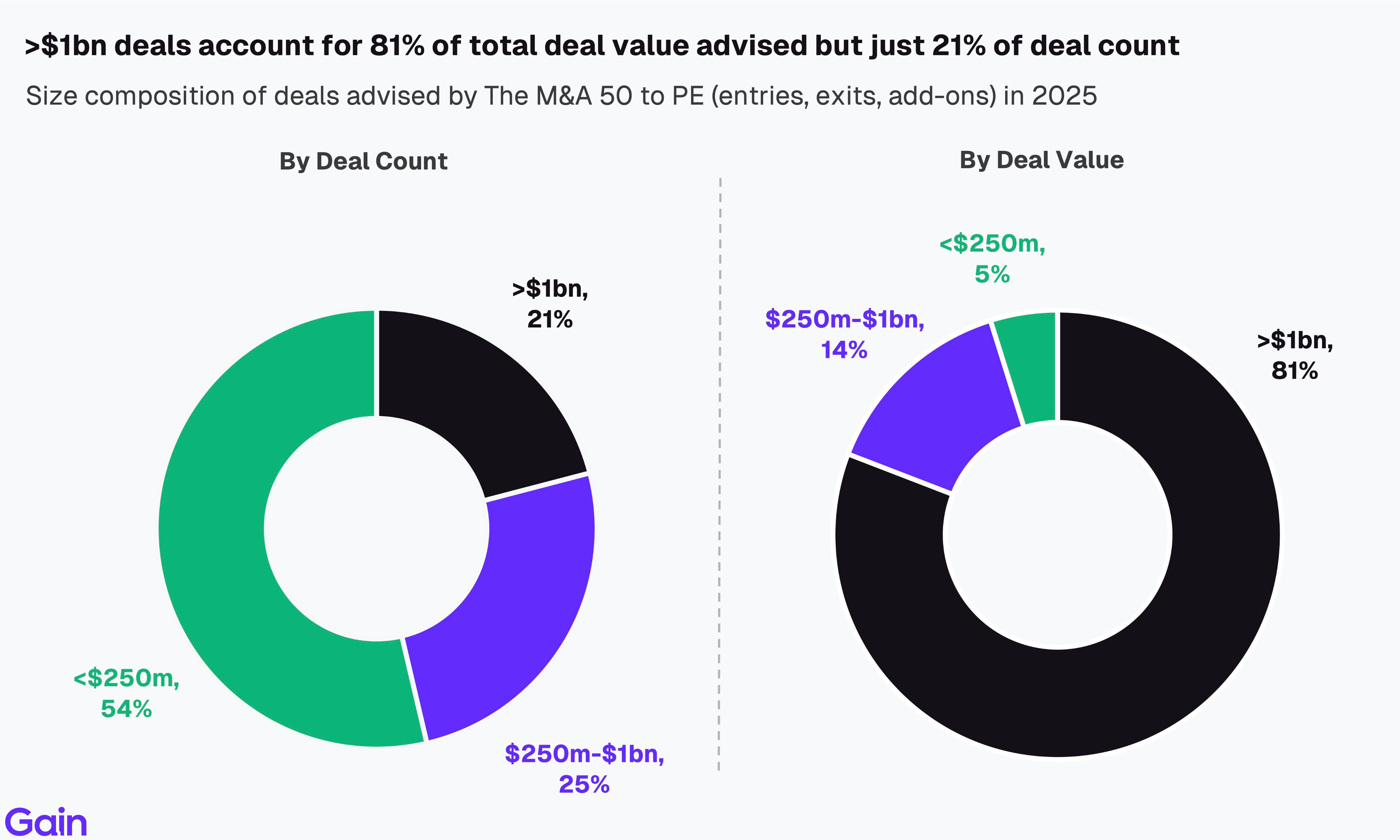

Large-cap deals (>$1bn) account for 81% of total deal value but are just 21% of advised transactions. This concentration means a small number of deals drives the bulk of the advisory fee pool. The lower mid-market (<$250m) dominates by count at 54%, yet contributes only 5% of value.

Chapter 02: Top 30 Insights

By Deal Size

Houlihan Lokey leads PE M&A advisory activity by deal count with 187 transactions, well ahead of Lincoln International (133) and Jefferies (126). Overall, US-based firms dominate the advisory activity, by count, accounting for 18 of the top 30 advisors. Rothschild & Co (115) is the most active non-US advisor.

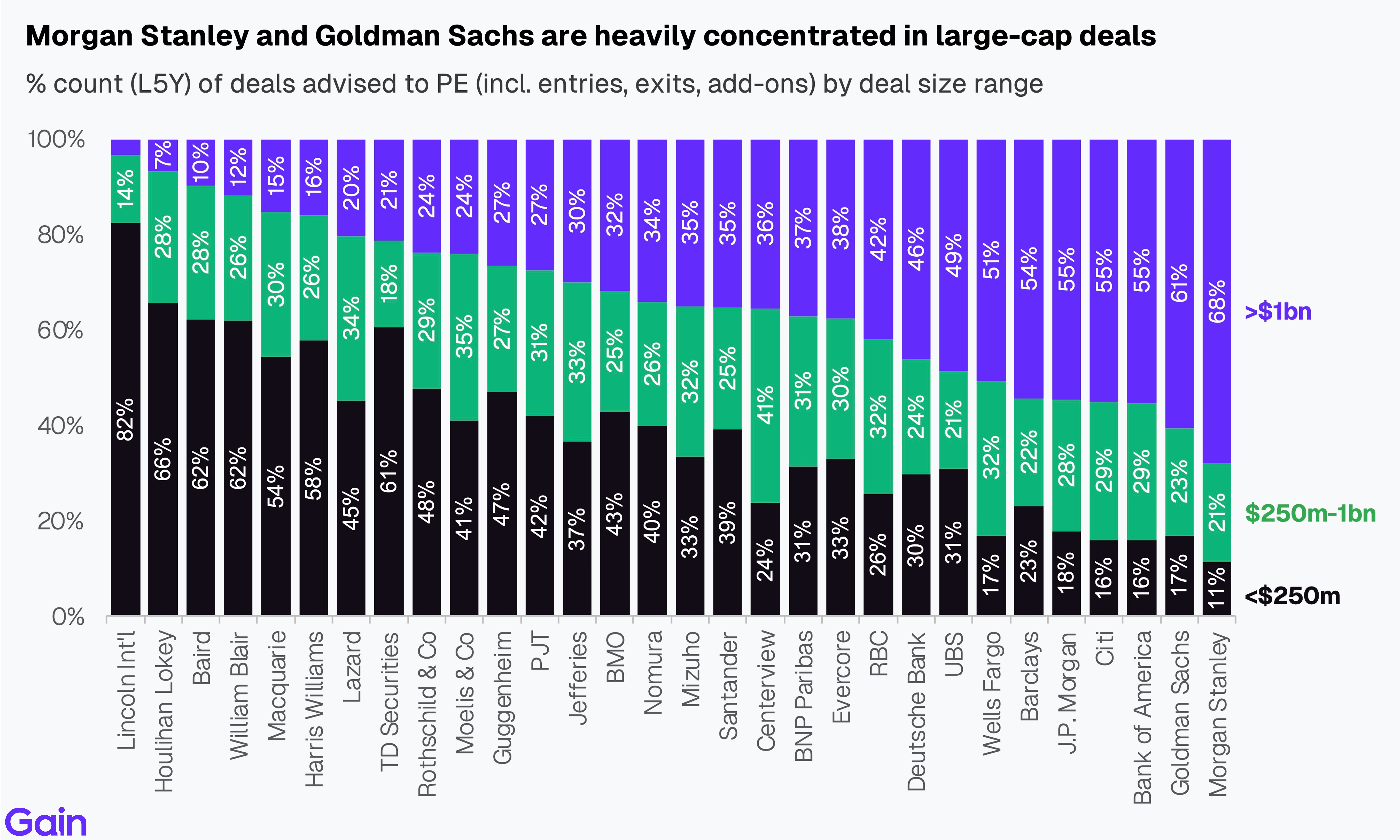

Morgan Stanley (68%), Goldman Sachs (61%), Bank of America (55%), Citi (55%) and J.P. Morgan (55%) are heavily concentrated in large-cap deals (>$1bn deal value), reflecting their bulge-bracket status. Lincoln International and Houlihan Lokey, in contrast, skew towards mid-market, with over 65% of advised volume in deals under $250m in EV. Advisors like Rothschild & Co, Jefferies, Evercore, and Lazard are more balanced, with a broader mix of deal sizes.

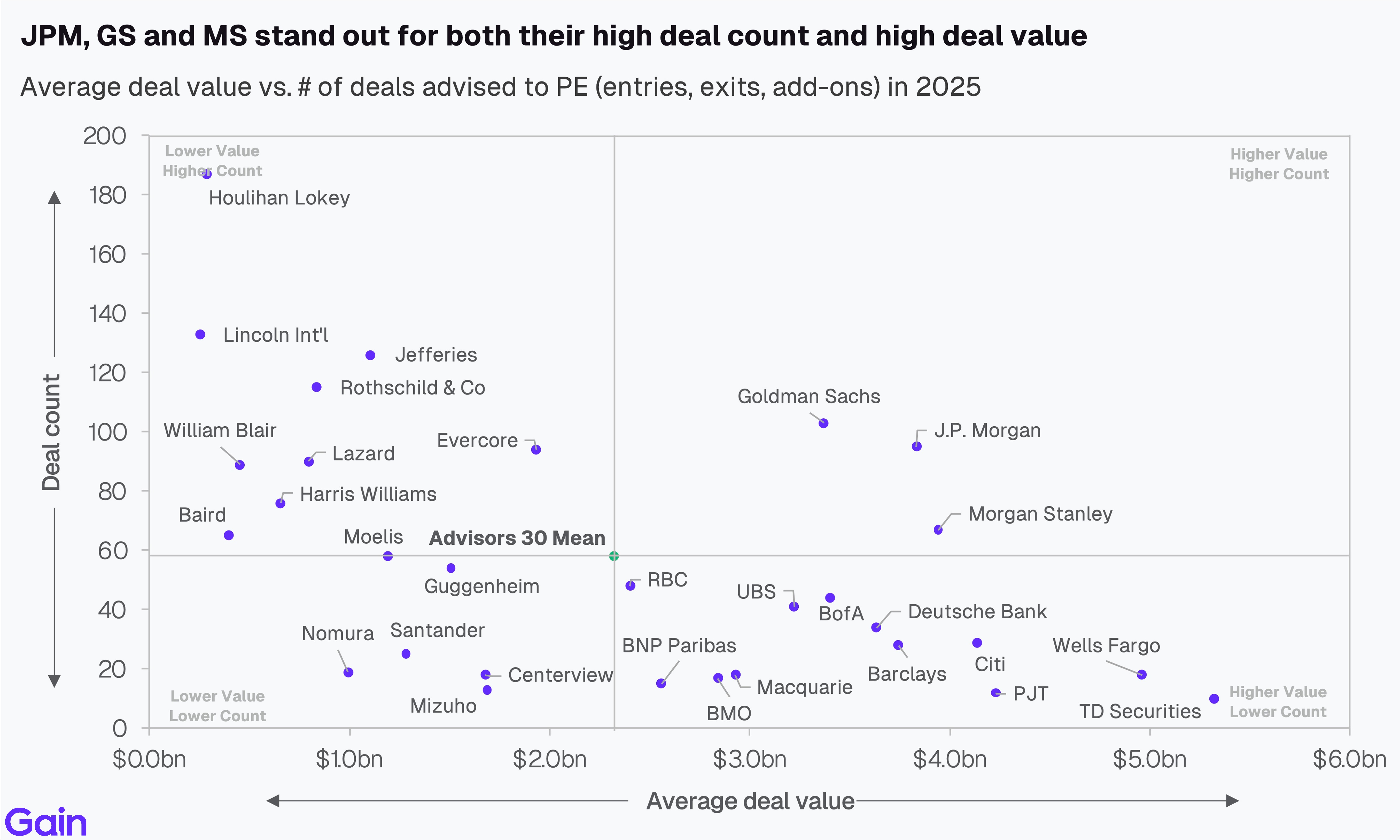

J.P. Morgan, Goldman Sachs, and Morgan Stanley stand out for both deal count and total deal value. Houlihan Lokey, Lincoln International, and Jefferies exceed or match them on count but have lower deal values on average.

By Sector & Region

Most large advisors advise across all sectors, though some specialize. Macquarie Group and Harris Williams skew toward Services (~40% of deal count), while William Blair, Barclays, and Evercore advise more on TMT deals. Finally, Centerview stands out for its Science & Health focus (36% of all its deals).

Most advisors in the M&A 50 are US-heavy, with over 60% of their deal count coming from that market. A few advisories stand out for their European focus: Rothschild & Co and BNP Paribas’s concentration in France (42% and 40% of their deals, respectively), Santander in Iberia/Italy (37%), and Macquarie in UK&I (20%). Canadian advisors such as RBC, TD Securities, and BMO also have a higher concentration of domestic deal flow.

By Deal Type

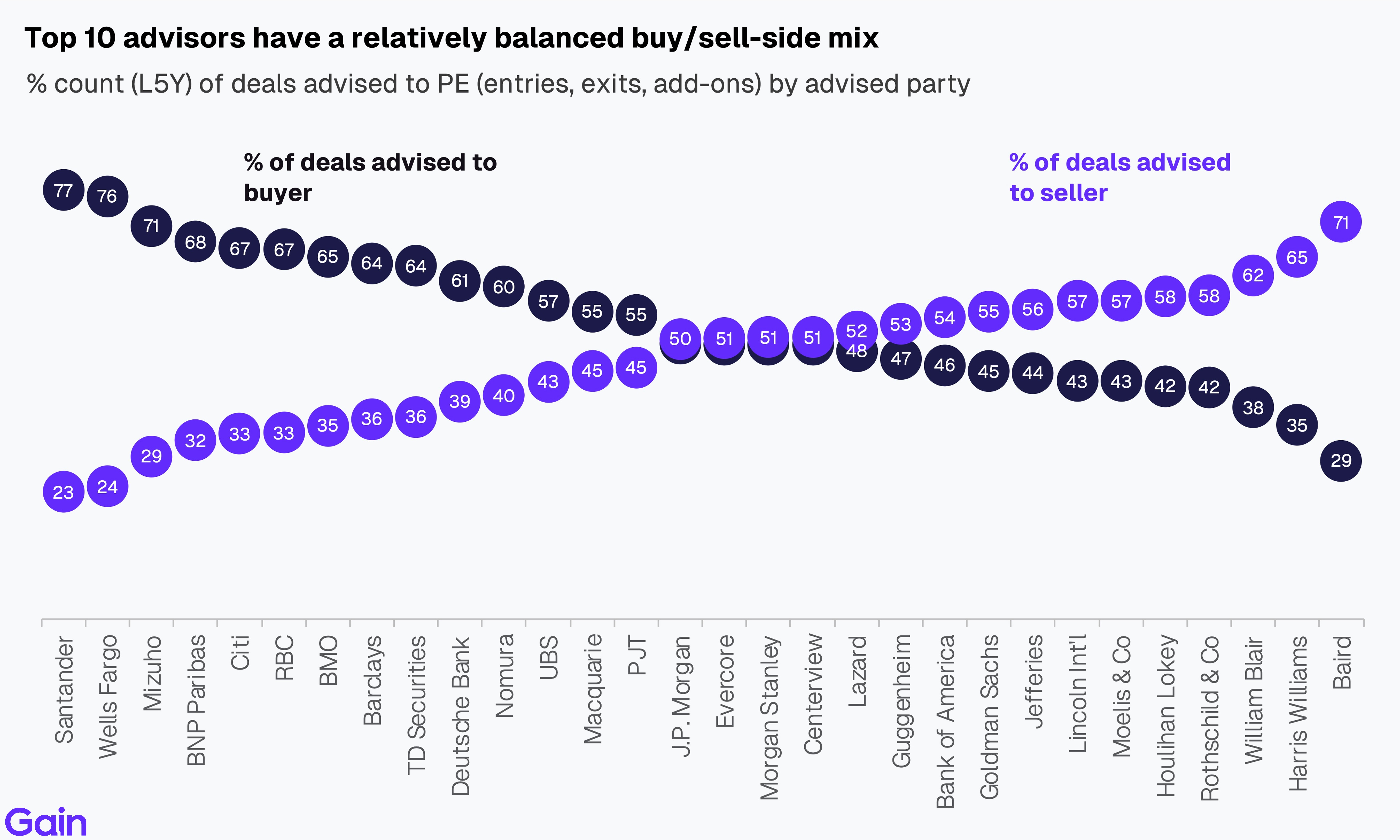

Most top advisors have a relatively balanced buy/sell mix, though a few mandate skews exist. Baird (71% sell-side), Harris Williams (65%), and William Blair (62%) skew toward sell-side mandates. This reflects their focus on running PE exit processes in the mid-market, which is more intermediated. Santander (77% buy-side), Wells Fargo (75%), and Mizuho (71%) sit at the other end, reflecting a stronger buy-side bias.

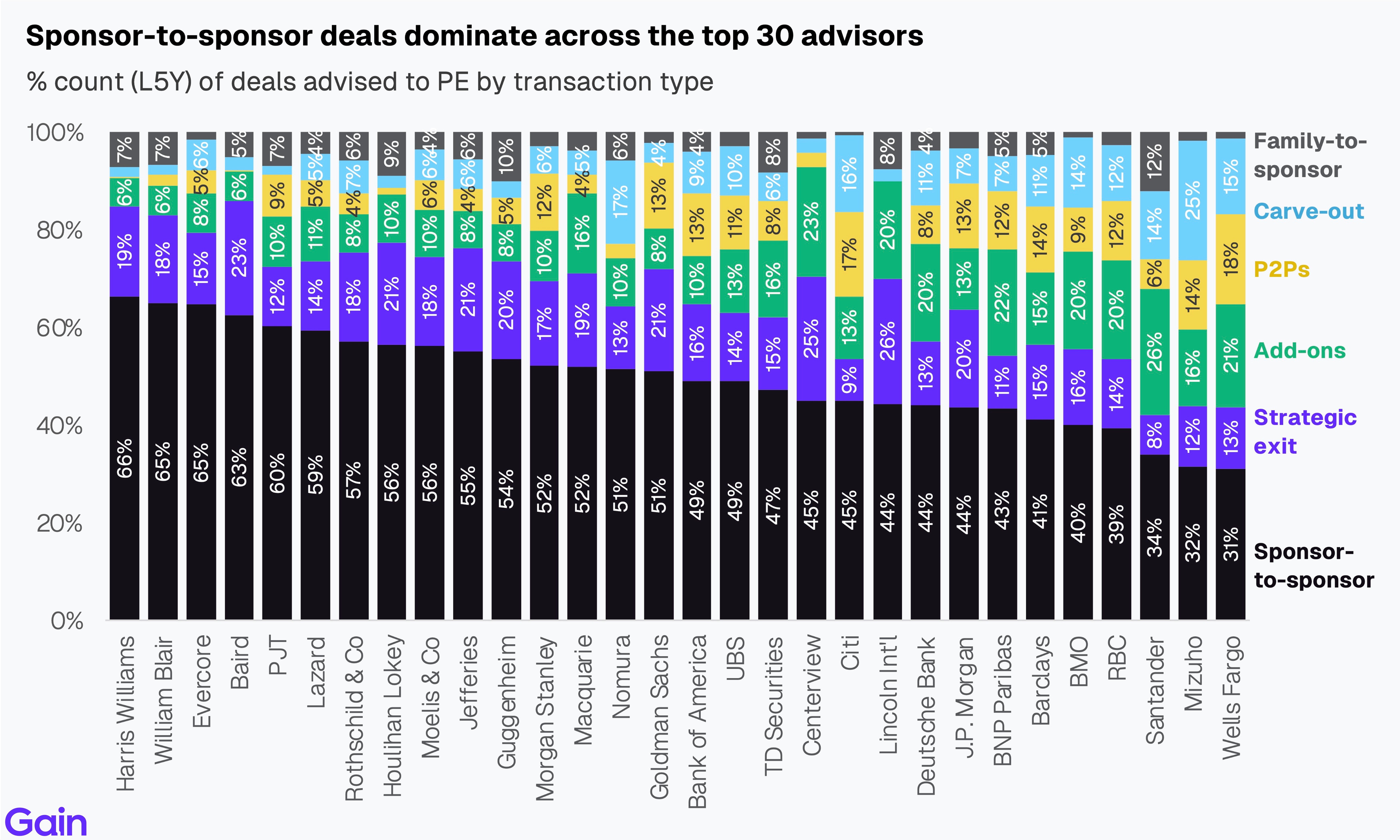

Sponsor-to-sponsor deals dominate across the top 30 advisors, accounting for the majority of advised count. Of active advisors, P2P activity is highest among bulge-bracket firms, led by Citi (19%), followed by Goldman Sachs, J.P. Morgan, Morgan Stanley, and Barclays. Carve-outs are most common at Citi (15%), Deutsche Bank (11%), and Barclays (11%), while Lincoln International (20%), Deutsche Bank (20%), and Centerview (23%) lead in add-ons.

Chapter 03: Ranking by Deal Size

This table showcases the top 25 M&A advisors to PE ranked by deal size (EV). Use the buttons to navigate between the large-cap (>$1bn), upper mid-market ($250m-$1bn), and lower mid-market (<$250m) rankings.

Top Advisors

The large-cap ranking is dominated by bulge-bracket firms, with J.P. Morgan, Goldman Sachs, and Morgan Stanley leading. In the upper and lower mid-market, Jefferies, Houlihan Lokey, Evercore, Lincoln International, and Rothschild & Co emerge as the leaders.

Larger deals attract more advisors per side, reflecting greater structural and execution complexity. 45% of large-cap deals (>$1bn) involve 2 or more advisors per side. Across transaction types, P2Ps are the most complex, with 40% involving two or more advisors, as regulatory, financing, and stakeholder complexities require broader advisory support.

Chapter 04: Regional Landscape

US advisory activity is dominated by US-headquartered advisors, holding a steady ~85% share across all deal sizes, with limited presence from international advisors. In Europe, the market is more fragmented between local and US advisors, with US firms commanding a rising share as deal size grows, reaching 54% for large-cap deals.

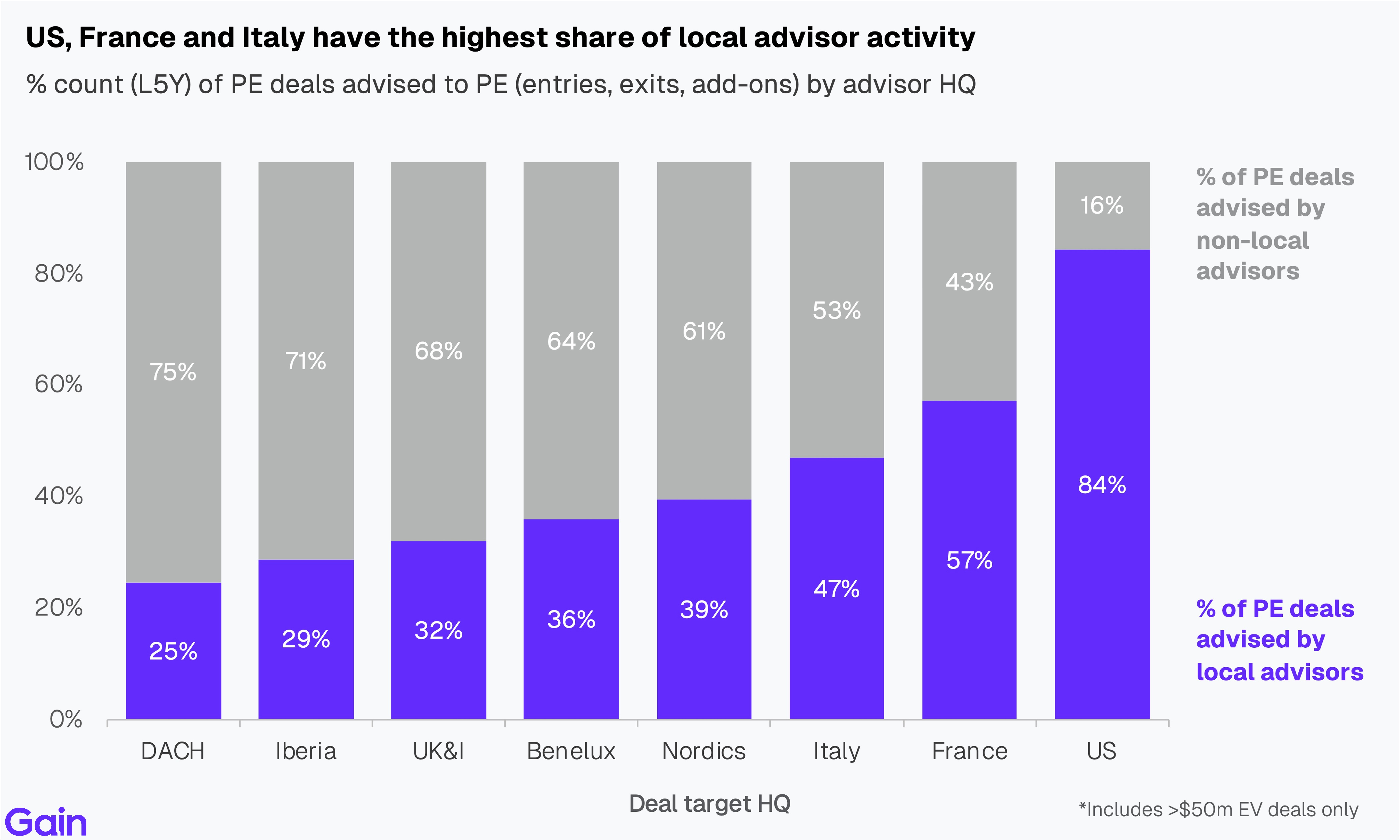

US, France and Italy have the highest share of local advisor activity. These markets benefit from a strong domestic advisor presence, including Rothschild & Co, BNP Paribas, Crédit Agricole, Investec, Société Générale, and Natixis Partners in France, and Intesa Sanpaolo, UniCredit, and Mediobanca in Italy. DACH (25%) and Iberia (29%), in contrast, are notably less local in their advisor mix.

Methodology

The M&A 50 ranks the largest M&A advisors advising to PE sponsors in 2025. The ranking is based on the total deal value advised to PE sponsors, including entries, exits, and add-ons. We exclude IPOs and ECM activity from the analysis.

An M&A advisor is eligible for a full deal credit if they specifically advised the PE or its portfolio company in a deal. We exclude from this analysis advisory roles to private individuals, non-PE-backed corporates, or public companies outside a PE context.

Deal value is based on the publicly reported enterprise value (EV), and is adjusted for the ownership stake that changed hands. Where deal EVs are undisclosed, we estimate them using an EV/EBITDA multiple approach.

We only include announced deals and exclude any rumoured transactions. We limit our analysis to deals with targets headquartered in Europe or North America.

We exclude from our ranking advisors with fewer than 5 deals advised to sponsors in 2025.