Industry research

Online food & grocery delivery services

Scope

US

Companies

56

Key takeaways

What is the scope of this industry report?

The US online food & grocery delivery services market comprises businesses that facilitate the digital ordering, payment and fulfillment of prepared meals, groceries and meal kits by connecting consumers with restaurants and retailers. Herein, meal delivery platforms provide on-demand access to restaurant-prepared food and typically manage last-mile delivery through owned or contracted courier networks. Meal kit delivery firms deliver pre-portioned ingredients and recipes directly to consumers' homes, primarily on a subscription basis. Additionally, grocery delivery providers enable consumers to purchase packaged foods, fresh produce and household essentials online, with picking, packing and last-mile delivery handled directly by the platform. Accordingly, we have segmented the US market into: (i) meals, (ii) meal kits and (iii) groceries.

What does the online food & grocery delivery services market landscape look like in the US?

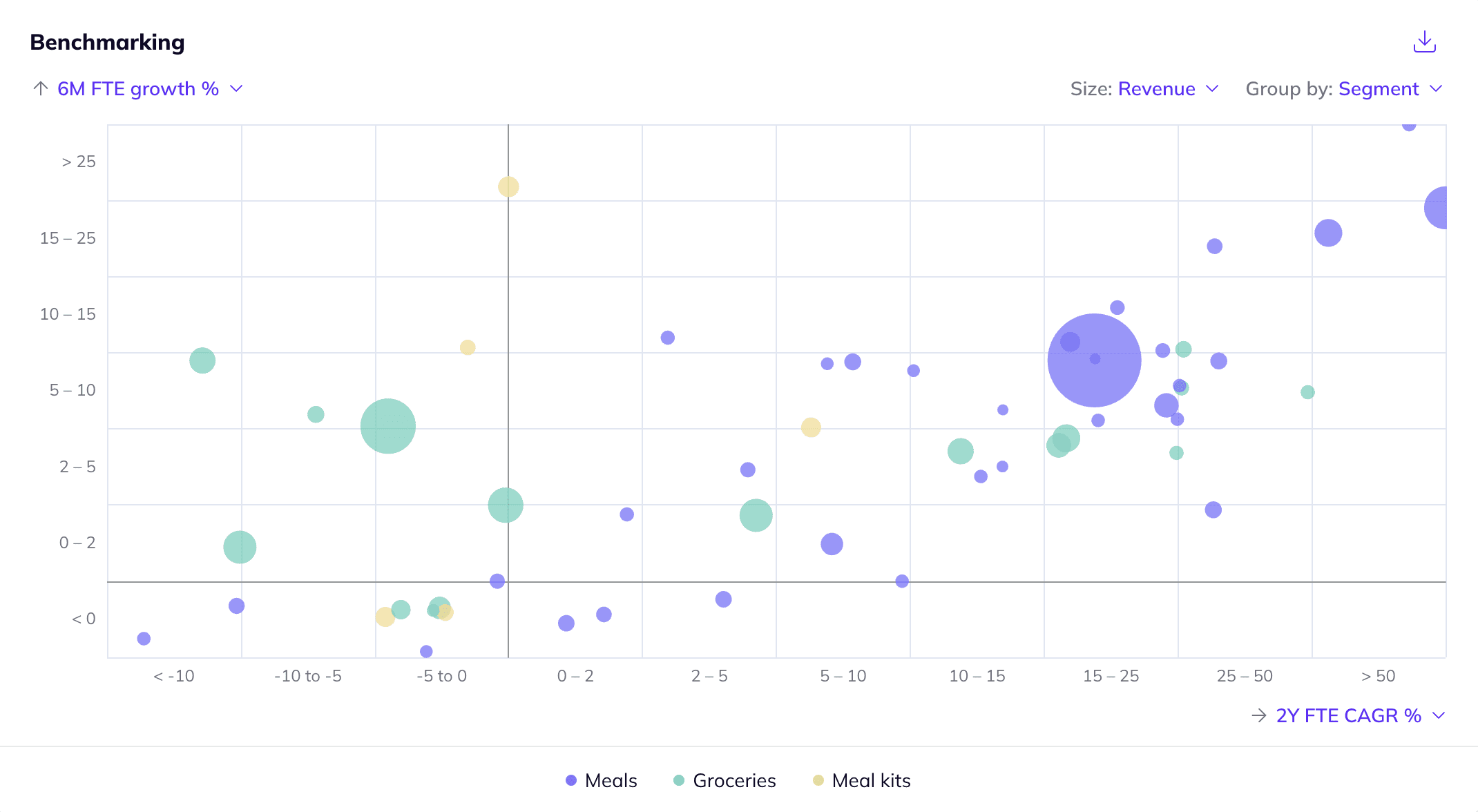

The US online food & grocery delivery services market is highly consolidated across all segments, with a small number of scaled platforms controlling the majority of order volumes. In meal delivery, DoorDash dominates with ~67% market share in 2024, followed by Uber Eats (US; Uber) at ~23%. Similarly, grocery delivery is led by Instacart with ~58% market share, while the meal kit segment is led by HelloFresh Group (DE), Home Chef (US; Kroger), Blue Apron (Wonder) and Sunbasket, collectively accounting for >70% of the market in 2024. Some of these large players continue to expand their (international) presence through strategic acquisitions (e.g. DoorDash's acquisition of Deliveroo). Meal and grocery delivery services platforms face competition from drone-based delivery players such as Zipline (US), Wing (US; Alphabet) and Flytrex (IL). At the same time, they also compete with large supermarket chains such as Walmart (US), Whole Foods Market (US; Amazon) and Kroger that leverage extensive store networks, established supply chains and omnichannel fulfillment capabilities, as well as restaurant-owned delivery channels (e.g. Domino’s) using proprietary apps and delivery networks to bypass platform commissions. To compete, the long tail tends to specialize in a particular niche. For example, Locale offers healthy, high-protein meals with low sugar, while Hungry Harvest focuses on farm-to-consumer produce delivery.

What is the level of investor activity in the US's online food & grocery delivery services industry?

Investor-led interest has been significant, with ~67% of identified assets being backed by financial sponsors (as of February 2026). Investors are primarily attracted by the market's favorable long-term outlook on the back of (i) an increase in consumer demand for digital-first convenience and time savings, (ii) structurally improved unit economics driven by automation and AI-enabled logistics and (iii) the evolution of platforms into multi-category marketplaces, which expands total addressable spend per user and increases order frequency. On the other hand, deterring factors include (i) increased competition from non-pure-play entrants such as large supermarket chains and drone-based delivery firms, which pressure commission rates and limit market share expansion, (ii) stricter labor regulation and worker classification requirements that compress per-order margins and (iii) rising delivery, service and platform fees that elevate total order costs and shift consumers toward in-store dining.

What are the key ESG considerations in the US's online food & grocery delivery services industry?

ESG topics in the US online food & grocery delivery services industry primarily relate to environmental and social challenges. Herein, environmental concerns stem mainly from carbon emissions driven by inefficient last-mile logistics, food waste from spoilage and excess purchasing and plastic waste generated by single-use packaging. To mitigate these impacts, incumbents pursue fleet electrification, routing optimization, surplus food redistribution initiatives and increased use of recyclable or returnable packaging. From a social perspective, worker safety and gig worker compensation remain core concerns. To address these issues, incumbents have introduced in-app safety features and compliance measures to improve the protection of delivery workers. Separately, regulatory scrutiny has increased around courier pay, account deactivations and broader platform labor practices.

Company benchmarking

Market growth

Statista (December 2025) forecasts the US online food delivery market to grow from ~$473.2bn in size in 2026 to ~$610.0bn by 2030 (+6.6% CAGR 2026-2030)

The global online grocery market was valued at ~$96.3bn in 2023 and is projected to reach ~$120.0bn by 2028 (+4.5% CAGR 2023-2028; Supermarket News, April 2024)

Positive drivers

Rising consumer demand for digital-first convenience, ease of access and time savings will drive growth in the online food & grocery delivery services market. To illustrate, Deloitte's grocery consumer survey indicates that ~52% of respondents prioritize convenience in grocery and food purchasing, particularly among younger consumers and busy urban professionals (PWC, June 2025; Deloitte, September 2024)

The emergence of automation and AI adoption in last-mile delivery and warehouse operations will lower unit delivery costs and increase order throughput. According to DHL, the use of AI in last-mile delivery can improve operational efficiency by ~30–50 % through route optimization, real-time tracking and predictive analytics. Additionally, the emergence of drone delivery supports market growth through faster delivery times and lower fulfillment costs (DHL, September 2025; 42Signals, September 2025; Deloitte, December 2024)

The evolution of online food delivery platforms into multi-category marketplaces across restaurant, grocery, alcohol, retail and everyday household goods represents a positive growth driver for the US market. This shift enables platforms to capture a larger share of everyday consumption, as broader category coverage expands total addressable spend per user and increases order frequency (CloudKitchens, April 2025; Deliverect, August 2024)

Negative drivers

The entry of non-pure-play competitors, including large supermarket chains (e.g. Walmart) and drone-based delivery firms, intensifies competitive pressure in the US online food & grocery delivery market. Large supermarket chains leverage scale and existing omnichannel infrastructure to secure lower commission rates, while drone-based delivery players benefit from lower delivery costs due to reduced labor intensity, increasing price pressure and constraining market share expansion for pure-play online food & grocery delivery platforms (42Signals, September 2025; Grocery Dive, March 2024)

Increased labor regulation, worker classification and compliance requirements compress margins for online food & grocery delivery platforms. To illustrate, in New York City, increases in mandated delivery worker wages have materially affected platform profitability, which prompted structural adjustments to pricing and cost models (Nelson Mullins, May 2025; DoorDash, October 2024; New York Post, July 2024)

Higher delivery, service and platform fees, introduced by operators to improve unit economics and offset rising labor and regulatory costs, have increased total order prices for consumers. As full order costs become more transparent at checkout, consumers prefer in-store dining, which reduces order frequency and caps long-term demand expansion across digital food delivery platforms (CNBC, July 2024; Restaurant Business, February 2023)

Fill out the form to request your copy of the Online food & grocery delivery services industry report

With the full report, you’ll gain access to:

Detailed assessments of the market outlook

Insights from c-suite industry executives

A clear overview of all active investors in the industry

An in-depth look into 56 private companies, incl. financials, ownership details and more.

A view on all 296 deals in the industry

ESG assessments with highlighted ESG outperformers

Discover hundreds of niche industry reports on Gain

Deep dive into additional industries to understand their market outlook, positive and negative drivers, and more!