Industry research

Fluid Management Systems

Scope

US

Companies

55

Key takeaways

What is the scope of this industry report?

The US fluid management systems market comprises businesses that develop and manufacture equipment used in the transmission, regulation, control and treatment of fluids. Core products include pumps, filters, valves, actuators, sensors, meters, fluid connectors and integrated control systems that help move, separate, monitor and manage liquids or gases within operating workflows. Offerings range from standardized components used in repeatable applications to customized or engineered systems designed for specific pressure, flow, material compatibility, purity, safety or regulatory requirements. Key end-markets include water and wastewater, food and beverage, pharmaceuticals, chemicals, oil and gas, power generation, automotive, general industrials, as well as building infrastructure.

Accordingly, we segmented the market by product focus into:

Generalist,

Pumps,

Filters.

What does the Fluid Management Systems landscape look like in the US?

The US fluid management systems market remains fragmented, reflecting the breadth of component categories, fluid types and end-market applications. Larger players expand market share through broad, multi-technology product portfolios that serve diverse end-market requirements, extensive distribution networks, manufacturing scale, deep positions in regulated and compliance-sensitive niches, custom engineering for client-specific applications, as well as hardware built for harsh operating environments. To compete, smaller players focus on proprietary designs and performance requirements that address specific applications. Across the market, competition extends beyond identified players, as international specialists (e.g. MANN+HUMMEL; DE) and large diversified industrial companies (e.g. Crane Company; US) offer overlapping pumps, filtration systems and flow-control products as part of broader industrial equipment portfolios. Consolidation in the market is driven by fragmented subsegments, attractive aftermarket economics and the push to expand product breadth across broader flow-control platforms, with M&A activity increasing to ~114 deals YTD through November 2025, up from ~97 in the prior-year period (Capstone Partners, December 2025).

What does the Fluid Management Systems market landscape look like in the US?

Sponsor-led interest has been moderate, with ~39% of identified assets being investor-backed (May 2026). Broader flow-control investor activity indicates selective sponsor appetite for scalable assets with strong end-market demand visibility, as platform acquisitions rose by ~25% YoY in 2025 and add-on acquisitions increased by ~83% to 33 deals YTD through November 2025, indicating continued traction for roll-up strategies (Capstone Partners, December 2025).

Herein, interest mainly stems from:

Water infrastructure repair and upgrade activity driven by aging assets, which supports replacement and new installations of fluid-control products,

Tightening federal standards across compliance-critical end-markets, which drive non-discretionary demand as operators upgrade treatment infrastructure to remain compliant,

Increasing adoption of smart fluid management, which favors sensor-enabled flow-control systems.

Deterring factors for investment include:

Escalating tariffs on raw materials and imported components, which increase input costs and delay procurement decisions,

Commoditization in standard fluid-management systems, which exposes players to heightened low-cost competition, price erosion and margin pressure,

Skilled-labor constraints, which raise labor costs, extend lead times and slow project delivery.

What are the key ESG considerations in the US Fluid Management Systems?

ESG topics primarily revolve around environmental and social risks. Environmental concerns primarily stem from the high energy consumption of continuously operating fluid management systems. Additionally, significant impacts arise from manufacturing emissions during machining, casting and fabrication, as well as the heavy water consumption and wastewater generation associated with testing, surface treatment and chemical cleaning. To address this, incumbents develop energy-efficient equipment, intelligent monitoring systems and predictive maintenance technologies, while also investing in energy-footprint reduction, lower-carbon product applications, closed-loop water systems and recycling initiatives. Social considerations mainly relate to occupational health and safety risks, as workers face exposure to hazardous chemicals and heavy machinery. To mitigate these risks, players strengthen safety protocols, deploy automation, standardize safety governance and implement employee-led safety programs.

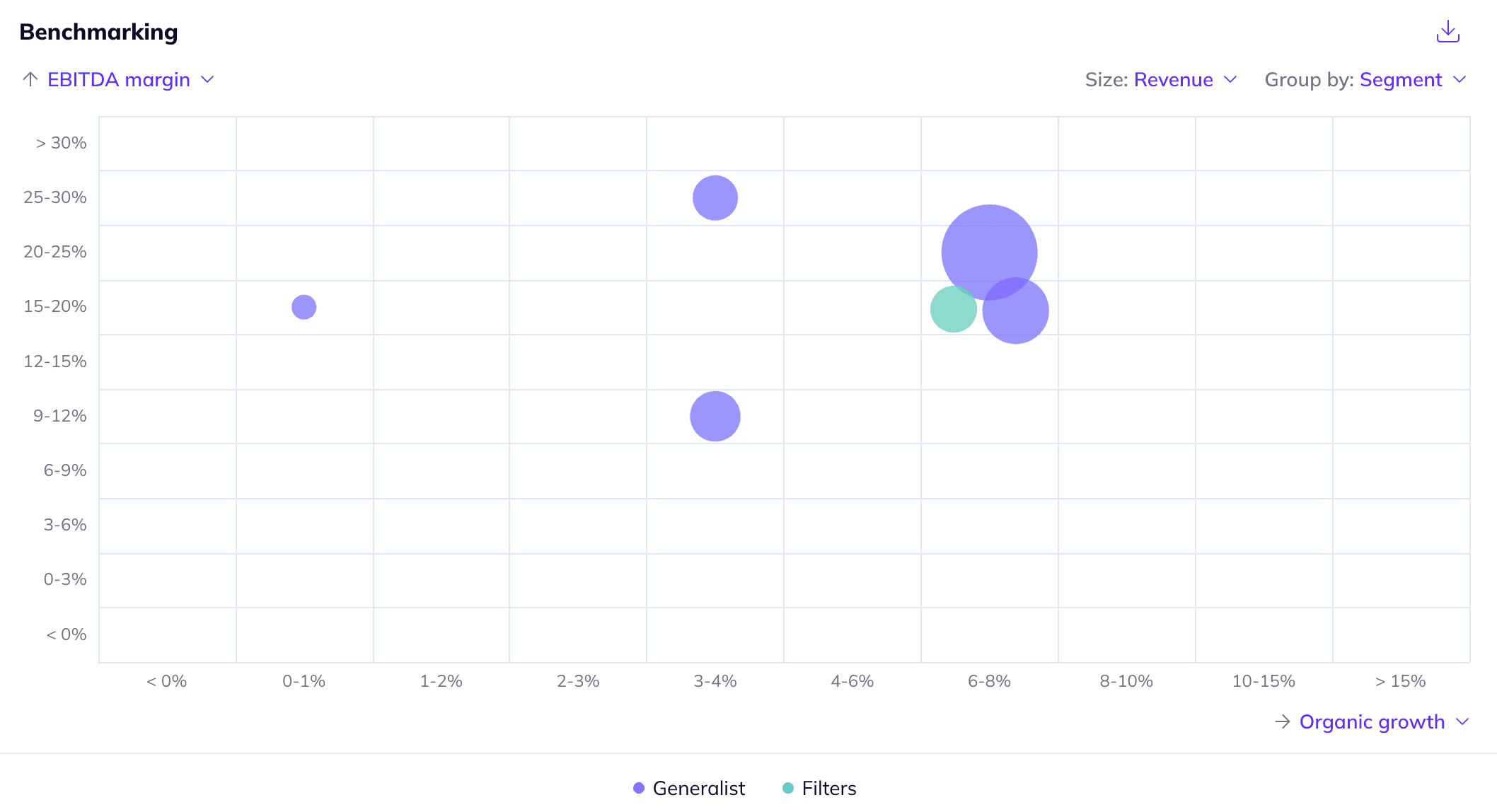

Company benchmarking

Market growth

According to Harris Williams (September 2024), the global flow control market was valued at ~$240.0bn in 2023 and is anticipated to grow to ~$340.0bn by 2030 (+5.1% CAGR 2023-2030)

Technavio (November 2024) expects the US sanitary pumps market to grow from ~$344.7m in 2023 to ~$405.3m in 2028 (+3.3% CAGR 2023-2028)

Positive drivers

Aging water networks, drought stress and chronic underinvestment in drinking water, wastewater and stormwater infrastructure will accelerate public and private infrastructure upgrades, thereby supporting replacement cycles and new installations across water projects. To illustrate, federal assessments project that repairing and modernizing US water infrastructure will require ~$3.4tn in CAPEX over the next 2 decades (The Value of Water, April 2026; EPA, March 2026; Governing, November 2025; Pew, September 2024)

Tightening federal standards across compliance-critical end-markets are driving non-discretionary demand for filtration and fluid-management systems, as operators replace and retrofit treatment infrastructure to remain compliant. For context, the EPA’s 2024 PFAS drinking-water rule set legally enforceable maximum contaminant levels for PFOA and PFOS at ~4 parts per trillion, while drinking-water utilities are expected to spend ~$13.5bn on PFAS retrofits between 2023-2030, primarily through granular activated carbon filtration (EPA, May 2026; Smart Water Magazine, January 2025)

Smart fluid management adoption strengthens demand for sensor-enabled flow-control systems as end-users prioritize real-time monitoring, leak detection, predictive maintenance and automated flow optimization. These systems continue to help reduce maintenance costs, minimize unplanned downtime and extend asset life across fluid handling applications (Environmental Finance Center Network, January 2026; Pumps & Systems, March 2025; Pumps & Systems, November 2024)

Negative drivers

Tariff-driven input cost inflation is squeezing profit margins and delaying procurement decisions for fluid management systems. This is largely driven by the updated US Section 232 framework, which assesses tariffs against the full customs value of covered metal imports, imposing a ~50% tariff on standard steel, aluminum and copper articles, as well as a ~25% tariff on specific derivative products (White & Case, April 2026; AMT, May 2025)

Commoditization in standard fluid-management systems, such as basic pumps, filter housings and routine filtration products, exposes the market to heightened competition from low-cost manufacturers. Chinese manufacturers hold a significant presence in the US market, accounting for ~14% of total US liquid pump imports and ~9% of centrifuge and filtering/purifying machinery imports. As buyers in less regulated, non-mission-critical applications have greater supplier choice, pricing power may weaken for US manufacturers and limit their margins (Trading Economics, May 2026; World's Top Exports, February 2026, Deloitte, October 2024)

A tight skilled-labor market constrains manufacturing capacity, field service availability and equipment installation. The US Chamber of Commerce reported that durable goods manufacturing had ~313k unfilled job openings, highlighting persistent hiring gaps in production-heavy sectors. Limited availability of machinists, welders, technicians and maintenance workers can raise labor costs, extend lead times and slow project delivery for fluid control systems (US Chamber, February 2026; ORF America, December 2025; Deloitte, April 2024)

Fill out the form to request your copy of the Fluid Management Systems industry report

With the full report, you’ll gain access to:

Detailed assessments of the market outlook

Insights from c-suite industry executives

A clear overview of all active investors in the industry

An in-depth look into 55 private companies, incl. financials, ownership details and more.

A view on all 98 deals in the industry

ESG assessments with highlighted ESG outperformers

Discover hundreds of niche industry reports on Gain

Deep dive into additional industries to understand their market outlook, positive and negative drivers, and more!