Industry research

Sports Brands

Scope

Europe

Companies

128

Key takeaways

What is the scope of this industry report?

The European sports brands market comprises businesses involved in the design, manufacturing, marketing and sale of sports apparel, sports equipment and fitness equipment. End customers include individual consumers, served directly ("D2C") and through third-party retailers, as well as business buyers (e.g. sports clubs, gyms, schools, federations).

We segmented the market according to players' product offerings:

Sports & outdoor apparel,

Sports equipment,

Fitness equipment.

What does the Sports Brands market landscape look like in Europe?

The European sports and outdoor market shows distinct competitive dynamics across segments. Sports apparel is the most contested, with the long-standing Nike–adidas duopoly eroded by scaled challengers (e.g. On, Lululemon) and category specialists (e.g. Arc'teryx, Hoka) now capturing the majority of segment economic profit through product innovation, niche positioning, community-led marketing and reclaimed wholesale shelf space. Notably, incumbents have been reversing the D2C push and returning to wholesale under cost and customer-acquisition pressure, while nearshoring (e.g. Turkey, Bulgaria) is gaining strategic momentum in response to tariffs and supply-chain risks in Asian hubs. However, near-term execution continues to lag the strategic intent. Sports equipment remains structurally fragmented along sport-specific niches, with consolidation happening through carefully assembled multi-brand portfolios or single-brand category extensions rather than horizontal roll-ups. Fitness equipment is the most concentrated, riding strong tailwinds from rising health-consciousness and gym participation across Europe, with hardware being commoditised and competition shifting toward connected hardware and software, AI-driven personalised training and B2B corporate-wellness subscription models.

What does the Sports Brands landscape look like in Europe?

Sponsor-led interest in sports brands has been moderate, with ~43% of identified assets being backed by financial sponsors (May 2026).

Investors are primarily attracted by:

The rise of active lifestyle as a personal identity, along with a rebound in gym attendance,

Tech-enabled platforms in fitness equipment supporting recurring revenue,

Increasing use of celebrity collaborations extending the addressable market beyond core athletic users into new lifestyle segments.

On the other hand:

Tariff uncertainty and Asian sourcing exposure pressuring margins and raising near-term capital needs for supply chain reconfiguration,

Higher compliance costs due to stringent EU sustainability regulations,

Cautious consumer sentiment compounded by second-hand adoption shifting volume away serve as key deterrents for investors.

What are the key ESG considerations in the European Sports Brands industry?

ESG topics mainly concern environmental and social matters. Environmentally, sportswear's heavy reliance on polyester and other synthetics drives carbon-intensive production and microplastic pollution. Identified players mitigate this by shifting toward recycled, renewable and lower-emission materials. Moreover, Asia-concentrated manufacturing and long-haul logistics push emissions overwhelmingly upstream into Scope 3. Incumbents aim to address this issue through supplier energy transition and logistics decarbonisation (e.g. marine biofuel). On the social side, the same Asian sourcing concentration raises risks around labour conditions and supply-chain transparency, which players aim to mitigate through independent third-party audit frameworks.

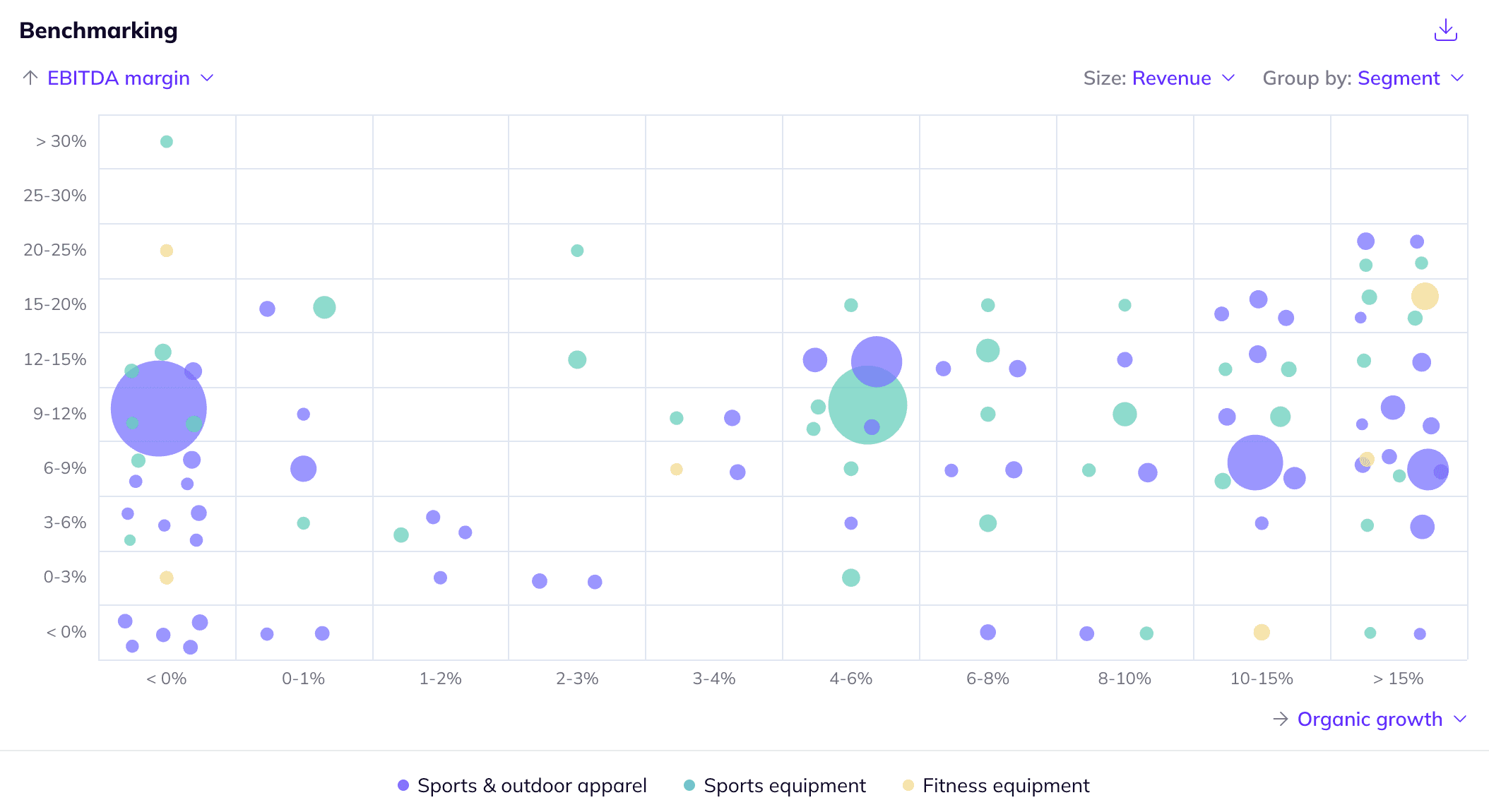

Company benchmarking

Market growth

McKinsey & Company (March 2025) estimates the Western and Eastern European sportswear market generated ~$86.0bn in retail sales in 2024 and forecasts it to reach ~$111.0bn in 2029 (+5.2% CAGR 2024-2029)

The European exercise equipment market is estimated to grow from ~€6.4bn in sales in 2026 to ~€7.5bn in 2030 (+3.8% CAGR 2026-2030; Statista, September 2025)

Positive drivers

Fitness has become core to consumer identity, with ~51% of physically active consumers and ~55–60% of Gen Z and Millennials viewing it as integral to self-image. This is reinforced by a post-pandemic rebound in gym attendance across Europe and a growing tendency for sportswear to feature in everyday wardrobes, driving demand growth for both apparel and equipment players (Athletech News, April 2025; McKinsey & Company, March 2025)

Tech-enabled platforms emerge as a structural moat in fitness equipment, with providers layering software, personalised training, smart devices and corporate subscriptions on top of otherwise commoditised hardware. Players combining hardware with connected services benefit from recurring revenue, higher switching costs and stronger pricing power, supporting margin resilience (HCM, April 2025; TechCrunch, September 2024)

European sports & outdoor apparel brands increasingly turn to celebrity collaborations, as seen in On's partnership with Zendaya to co-create a footwear and apparel collection and PUMA Group's collaboration with K-pop star Rosé, who fronts the campaign for its H-Street sneaker. With lifestyle influencers now overtaking athletes in visibility, such partnerships extend the addressable market beyond core athletic users into new lifestyle segments (WWD, May 2026; On, April 2026; Fashion Network, August 2025)

Negative drivers

Ongoing tariff uncertainty across Asian manufacturing hubs creates margin pressure and price pass-through risks for European brands with heavy Asia sourcing and US exposure (e.g. ~21% of adidas' sales are generated in North America and ~66% for On). Additionally, the heavy reliance on Asia heightens supply chain resilience risks amid geopolitical volatility (e.g. Red Sea disruptions), driving near-term capital needs for supply chain reconfiguration (Statista, April 2026; SwissInfo, April 2025; The Business of Fashion, April 2025; McKinsey & Company, May 2024)

Increasingly stringent EU regulations, along with rising sustainability and product lifecycle requirements (e.g. restrictions on the destruction of unsold goods), are raising compliance and operational costs for sports apparel brands. At the same time, >50% of European consumers prioritise cost and value for money, limiting cost pass-through and pressuring margins (Innova Market Insights, April 2024; FESI, April 2024)

European consumer confidence has dropped to a 2-year low amid inflation in energy, food and housing. The resulting caution drives demand polarisation and squeezes mid-tier, less differentiated brands. Growing second-hand adoption further heightens headwind, shifting volume away from first-hand sales and forcing brands to build circular offerings at added operational cost (SGI Europe, March 2026; McKinsey & Company, July 2025; ISPO, May 2024)

Fill out the form to request your copy of the Sports Brands industry report

With the full report, you’ll gain access to:

Detailed assessments of the market outlook

Insights from c-suite industry executives

A clear overview of all active investors in the industry

An in-depth look into 128 private companies, incl. financials, ownership details and more.

A view on all 399 deals in the industry

ESG assessments with highlighted ESG outperformers

Discover hundreds of niche industry reports on Gain

Deep dive into additional industries to understand their market outlook, positive and negative drivers, and more!